How Car Insurance Deductibles Work

Car insurance deductibles are one of the most important yet misunderstood aspects of auto insurance in the United States. Many drivers choose a deductible amount without fully understanding how it affects their premiums, out-of-pocket costs, and overall financial protection.

A deductible can significantly change how much you pay both monthly and after an accident. Understanding how it works is essential for choosing the right car insurance policy and avoiding unexpected expenses when filing a claim.

This guide explains in detail what a car insurance deductible is, how it works, how it affects your premium, and how to choose the right amount based on your situation.

What is a car insurance deductible?

A car insurance deductible is the amount of money you must pay out of pocket before your insurance company pays for the remaining cost of a covered claim.

In simple terms, it is your share of the repair or replacement cost when you file a claim.

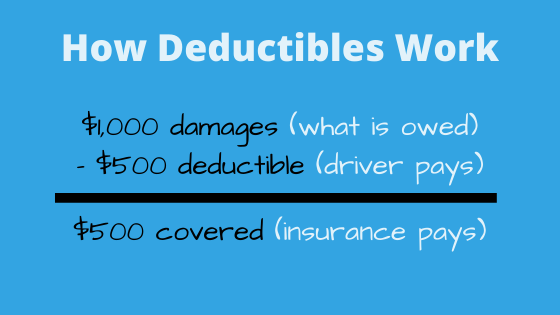

For example:

- Total repair cost: $2,000

- Deductible: $500

- Insurance payout: $1,500

You always pay the deductible first, and the insurance company covers the rest (up to your policy limits).

Deductibles typically apply to:

- Collision coverage

- Comprehensive coverage

Liability insurance does NOT usually have a deductible, because it covers damage to other people, not your own vehicle.

How deductibles work in real situations

When you get into an accident or your car is damaged, you file a claim with your insurance company.

Once the claim is approved, the insurance company determines the total cost of repairs or replacement. Before they pay anything, your deductible is applied.

This means:

- If damage is less than your deductible, insurance does not pay

- If damage is higher than your deductible, you pay the deductible and insurance covers the rest

For example, if your deductible is $1,000 and the repair costs $800, you will pay the full amount yourself and your insurance will not contribute.

Types of deductibles in car insurance

There are generally two main types of deductibles in auto insurance policies:

Fixed deductible

This is a set dollar amount chosen when you buy the policy, such as $250, $500, or $1,000.

Percentage-based deductible

Less common, this type is based on a percentage of your vehicle’s insured value. It is often used in specific cases like comprehensive coverage in high-risk areas.

For most drivers in the U.S., fixed deductibles are standard.

How deductibles affect your insurance premium

There is a direct relationship between deductibles and monthly insurance costs.

- Higher deductible → lower monthly premium

- Lower deductible → higher monthly premium

This happens because the deductible determines how much risk you are willing to take on.

If you choose a higher deductible, you are agreeing to pay more out of pocket in case of an accident, so the insurance company charges you less each month.

If you choose a lower deductible, the insurer takes on more risk, so your premium increases.

Common deductible amounts in the USA

Most drivers in the United States choose deductibles within a common range:

- $250 deductible (low out-of-pocket cost, higher premium)

- $500 deductible (most common option)

- $1,000 deductible (lower premium, higher risk)

- $2,000+ deductible (used for maximum savings on monthly cost)

The “best” deductible depends on your financial situation and risk tolerance.

When you pay the deductible

You only pay the deductible when you file a claim under a covered event.

Situations where you typically pay a deductible include:

- Car accidents (collision coverage)

- Theft or vandalism (comprehensive coverage)

- Weather-related damage like hail or flooding

However, if another driver is fully at fault and their insurance pays, you may not have to pay your deductible.

In some cases, your insurer may recover the cost from the at-fault party and reimburse your deductible later.

Deductible in collision vs comprehensive coverage

Most car insurance policies have separate deductibles for different types of coverage.

Collision deductible

Applies when your car is damaged in an accident involving another vehicle or object.

Comprehensive deductible

Applies to non-collision events such as theft, fire, or natural disasters.

In many cases, both deductibles are the same, but policyholders can choose different amounts depending on preference.

Choosing the right deductible amount

Selecting the right deductible is a balance between monthly affordability and out-of-pocket risk.

A lower deductible may be better if:

- You want predictable costs after an accident

- You do not have savings for unexpected repairs

- You drive frequently or in high-traffic areas

A higher deductible may be better if:

- You want to reduce monthly insurance costs

- You rarely file claims

- You can afford to pay more in case of an accident

There is no universally “best” deductible, only the one that fits your financial situation.

Deductibles and minor accidents

One important consideration is that deductibles often make small claims unnecessary.

For example:

- Repair cost: $600

- Deductible: $500

In this case, insurance would only pay $100, meaning it may not be worth filing a claim.

Many drivers choose higher deductibles to avoid frequent small claims that could potentially increase their insurance rates.

Do deductibles affect claim approval?

Deductibles do not affect whether a claim is approved. They only affect how much you pay when a claim is approved.

Your insurance company still evaluates:

- Fault

- Coverage eligibility

- Policy limits

The deductible is simply applied after approval.

Common misconceptions about deductibles

Many drivers misunderstand how deductibles work. Some common misconceptions include:

- Thinking deductible is paid monthly (it is only paid per claim)

- Believing deductible is paid to the insurance company (it is usually paid to the repair shop or deducted from payout)

- Assuming deductible applies to liability claims (it usually does not)

- Thinking lower deductible always saves money (it increases monthly premiums)

Understanding these details helps avoid confusion when filing a claim.

Deductibles and total loss situations

If your car is declared a total loss, the deductible is still applied.

For example:

- Car value: $10,000

- Deductible: $1,000

- Insurance payout: $9,000

Even in total loss cases, the deductible reduces the final payout amount.

Final thoughts

Car insurance deductibles play a major role in how much you pay for insurance and how much financial responsibility you take on after an accident.

Choosing the right deductible is a key decision that affects both your monthly budget and your financial protection in emergencies.

While higher deductibles reduce monthly premiums, they increase your risk in case of a claim. Lower deductibles provide more immediate protection but come with higher ongoing costs.

Understanding this balance is essential for building a car insurance policy that fits your needs and avoids unexpected financial stress.

Frequently Asked Questions

What is a deductible in car insurance?

It is the amount you pay out of pocket before your insurance covers a claim.

Do I pay the deductible every month?

No, only when you file a covered claim.

What is a good deductible amount?

Most drivers choose between $500 and $1,000 depending on budget.

Does liability insurance have a deductible?

Usually no, deductibles apply mainly to collision and comprehensive coverage.