How to Get Cheap Car Insurance in the USA

Car insurance in the United States can be expensive, and for many drivers it represents one of the largest recurring vehicle-related expenses. However, most people do not realize that insurance premiums are highly flexible and can often be significantly reduced by making strategic decisions.

Insurance companies calculate prices based on risk, but also on multiple adjustable factors such as coverage level, deductibles, driving behavior, and discounts. This means that two drivers with similar cars can pay completely different amounts for the same type of coverage.

This guide explains practical, proven strategies to get cheap car insurance in the USA in 2026 without sacrificing essential protection.

Why car insurance is expensive in the USA

Before learning how to reduce costs, it is important to understand why insurance prices vary so much.

Insurance companies base premiums on risk assessment, which includes:

- Likelihood of accidents

- Cost of vehicle repairs

- Medical costs in your area

- Driving history

- Location risk (state and ZIP code)

- Vehicle type and usage

In areas with high traffic density or high accident rates, premiums tend to be significantly higher. Similarly, newer or more expensive vehicles also increase insurance costs due to higher repair or replacement value.

1. Compare multiple insurance quotes

One of the most effective ways to get cheaper car insurance is to compare quotes from multiple providers.

Insurance companies do not all calculate risk the same way, which means prices for identical coverage can vary significantly between providers.

By comparing quotes, drivers can often find savings of hundreds or even thousands of dollars per year.

It is important to compare:

- Coverage limits

- Deductibles

- Included benefits

- Optional add-ons

Focusing only on price without comparing coverage can lead to underinsurance.

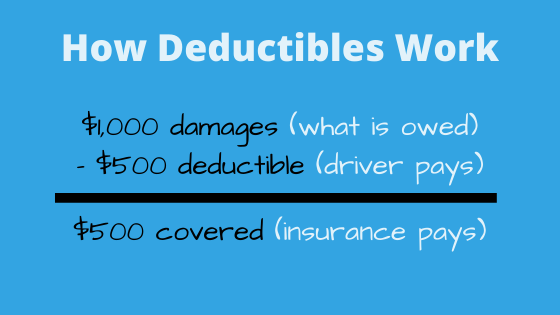

2. Increase your deductible

One of the simplest ways to reduce monthly premiums is to increase your deductible.

The deductible is the amount you pay out of pocket before your insurance covers a claim.

For example:

- Low deductible = higher monthly premium

- High deductible = lower monthly premium

Drivers who are confident in their driving or who rarely file claims often choose higher deductibles to reduce costs.

However, it is important to ensure you can afford the deductible amount in case of an accident.

3. Take advantage of discounts

Insurance companies in the USA offer a wide range of discounts that many drivers fail to use.

Common discounts include:

- Safe driver discount

- Multi-policy (bundling home and auto insurance)

- Good student discount

- Low mileage discount

- Military or professional discounts

- Vehicle safety feature discounts

These discounts can significantly reduce the final premium if properly applied.

4. Maintain a clean driving record

Your driving history is one of the most important factors in determining insurance cost.

Drivers with no accidents or traffic violations are considered low risk and typically pay lower premiums.

On the other hand, speeding tickets, accidents, or DUIs can significantly increase insurance costs for several years.

Maintaining a clean driving record is one of the most effective long-term strategies for cheap insurance.

5. Improve your credit score

In many U.S. states, insurance companies use credit-based insurance scores to calculate premiums.

Drivers with higher credit scores are often considered more financially responsible and less likely to file claims.

Improving your credit score can lead to:

- Lower monthly premiums

- Better insurance offers

- Increased eligibility for discounts

This makes credit management an indirect but powerful factor in reducing insurance costs.

6. Choose the right vehicle

The type of car you drive has a direct impact on your insurance cost.

Vehicles that are cheaper to insure usually have:

- Lower repair costs

- High safety ratings

- Low theft rates

- Moderate engine power

Sports cars, luxury vehicles, and expensive models generally cost more to insure due to higher risk and repair costs.

Choosing a practical and safe vehicle can significantly reduce insurance premiums over time.

7. Reduce unnecessary coverage

Many drivers pay for coverage they do not actually need.

For example:

- Older vehicles may not need full coverage

- Some add-ons may not provide real value for your situation

Reviewing your policy regularly can help eliminate unnecessary costs while maintaining essential protection.

However, it is important not to remove coverage that could expose you to high financial risk.

8. Drive less to pay less

Mileage is another factor used by insurance companies to calculate risk.

Drivers who spend less time on the road have a lower probability of accidents.

Ways to reduce mileage include:

- Using public transport when possible

- Working from home

- Carpooling

Some insurers even offer low-mileage discounts or usage-based insurance programs that track driving habits.

9. Consider usage-based insurance

Usage-based insurance (UBI) programs track driving behavior using mobile apps or devices installed in your vehicle.

These programs monitor:

- Speeding habits

- Braking behavior

- Mileage

- Driving times

Safe drivers can receive significant discounts based on their real driving performance instead of general statistical risk.

10. Bundle insurance policies

Bundling multiple insurance policies with the same provider is one of the easiest ways to save money.

Common bundles include:

- Auto + home insurance

- Auto + renters insurance

Insurance companies reward bundled customers with discounts because they are more likely to stay with the company long term.

11. Choose the right coverage level

Choosing the correct coverage level is essential for balancing cost and protection.

For example:

- Liability-only insurance is cheaper but less protective

- Full coverage is more expensive but offers broader protection

The right choice depends on:

- Vehicle value

- Financial situation

- Risk tolerance

Over-insuring or under-insuring can both lead to financial inefficiency.

Common mistakes that increase insurance costs

Many drivers unintentionally pay more for insurance due to simple mistakes:

- Not comparing quotes regularly

- Ignoring available discounts

- Keeping unnecessary coverage

- Failing to update policy after life changes

- Letting insurance auto-renew without reviewing it

Avoiding these mistakes can lead to significant long-term savings.

Final thoughts

Getting cheap car insurance in the United States is not about finding the lowest possible price, but about optimizing coverage based on your personal risk profile.

Insurance premiums are highly flexible and influenced by many factors, including driving behavior, vehicle choice, credit score, and coverage selection.

By actively comparing options, adjusting coverage wisely, and taking advantage of discounts, most drivers can significantly reduce their insurance costs without sacrificing essential protection.

The key is not to treat insurance as a fixed expense, but as a customizable financial product that can be optimized over time.

Frequently Asked Questions

What is the cheapest car insurance in the USA?

It depends on the driver, but liability-only policies with discounts are usually the cheapest.

How can I lower my car insurance quickly?

Increasing your deductible and applying discounts are the fastest methods.

Does my credit score affect car insurance?

Yes, in most U.S. states it can significantly impact your premium.

Is it safe to choose the cheapest insurance?

Not always. Low cost may mean lower coverage, so balance is important.