How to Read Your Car Insurance Policy (Without Confusion)

A car insurance policy is a legal contract that defines exactly what is covered, what is excluded, and how much protection you have in different situations. However, most drivers never fully read or understand their policy, which can lead to confusion when filing a claim or discovering unexpected limitations.

Insurance documents are often filled with technical terms, legal language, and complex structures that make them difficult to interpret. Understanding how to read your car insurance policy is essential if you want to avoid overpaying, missing important coverage, or being surprised after an accident.

This guide breaks down how a typical U.S. car insurance policy is structured, what each section means, and how to quickly identify the most important information.

What a car insurance policy actually is

A car insurance policy is a written agreement between you and your insurance company. It outlines:

- What risks are covered

- What is excluded

- How much the insurer will pay

- What your responsibilities are as the policyholder

In the United States, every driver who carries insurance has a policy document, whether digital or physical. This document is legally binding and determines how claims are handled.

The main sections of a car insurance policy

Most insurance policies in the U.S. follow a similar structure. Although wording may vary between companies, the core sections remain the same.

1. Declarations page

The declarations page (often called the “dec page”) is the summary of your entire insurance policy. It is the most important page because it contains the key details of your coverage.

It typically includes:

- Policyholder name and address

- Vehicle information (make, model, VIN)

- Coverage types and limits

- Deductibles

- Premium amount

- Policy start and end dates

This page gives you a quick overview of what your insurance includes without reading the full contract.

2. Coverage sections

This section explains in detail what your policy actually covers. Each type of coverage is listed separately with its limits and conditions.

Common coverage types include:

- Liability coverage

- Collision coverage

- Comprehensive coverage

- Uninsured/underinsured motorist coverage

- Medical payments or PIP (depending on the state)

Each coverage section specifies:

- What is covered

- Maximum payout limits

- Conditions for eligibility

Understanding this section is essential because it defines the financial protection you actually have.

3. Exclusions

Exclusions are one of the most important parts of any insurance policy. They describe situations where your insurance will NOT provide coverage.

Common exclusions include:

- Intentional damage

- Driving under the influence

- Using your car for commercial purposes (if not insured for it)

- Mechanical breakdowns

- Wear and tear

Many drivers skip this section, but it is critical because it defines the limits of your protection.

4. Conditions

The conditions section explains the rules you must follow for your insurance to remain valid.

This includes:

- How to file a claim

- Deadlines for reporting accidents

- Responsibilities after a loss

- Cooperation requirements during investigations

If you fail to meet these conditions, your claim may be delayed or denied.

5. Definitions section

Insurance policies include a glossary of terms used throughout the document. This section defines technical language such as:

- “Insured”

- “Premium”

- “Deductible”

- “Covered loss”

- “Liability”

Understanding these definitions helps avoid misinterpretation of the policy language.

Understanding coverage limits

Coverage limits define the maximum amount your insurance company will pay for a claim.

For example, liability coverage might be written as:

- $50,000 bodily injury per person

- $100,000 bodily injury per accident

- $50,000 property damage

These limits are extremely important because if damages exceed them, you are responsible for the difference.

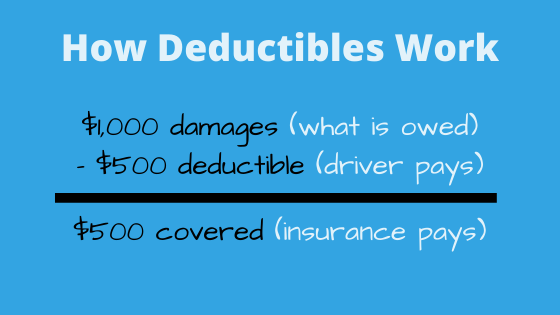

How deductibles appear in your policy

Deductibles are clearly listed in your declarations page and apply mainly to:

- Collision coverage

- Comprehensive coverage

Your policy will specify the exact deductible amount, such as $500 or $1,000.

This is the amount you must pay before the insurance company contributes to a claim.

What is not always obvious in a policy

Many important details are not immediately obvious when reading an insurance policy.

These include:

- Optional coverage that is not automatically included

- Sub-limits for specific types of claims

- Conditions that may reduce payout amounts

- Restrictions based on driver behavior or usage

This is why two policies that look similar on paper can offer very different real-world protection.

How to quickly check if you are properly covered

Instead of reading every word of the policy, you can focus on key areas:

First, check your liability limits. These determine your protection against lawsuits and third-party claims.

Next, review whether you have collision and comprehensive coverage. These determine whether your own vehicle is protected.

Then, check your deductibles to understand your out-of-pocket costs.

Finally, verify any optional coverages such as rental car reimbursement or roadside assistance.

Common mistakes when reading insurance policies

Many drivers make the same mistakes when reviewing their insurance documents:

- Only looking at the price and ignoring coverage details

- Not checking exclusions

- Assuming full coverage means everything is included

- Not reviewing policy renewal changes

- Ignoring coverage limits

These mistakes often lead to unexpected costs after accidents.

Why insurance policies are written in complex language

Insurance policies are legal documents designed to be precise and legally enforceable. Because of this, they use technical language to avoid ambiguity.

While this makes them harder to read, it also ensures that both the insurance company and the policyholder have a clear understanding of responsibilities and coverage terms.

Digital policies vs paper policies

Most insurance companies in the United States now provide digital policy documents.

Digital policies have advantages such as:

- Easier access via apps or websites

- Faster updates

- Search functionality to find terms quickly

However, the content remains the same as traditional paper policies.

Final thoughts

Reading a car insurance policy may seem complicated at first, but understanding its structure makes it much easier to interpret.

The key sections to focus on are the declarations page, coverage details, exclusions, and conditions. These determine what is actually covered, how much protection you have, and what responsibilities you must follow.

By taking the time to understand your policy, you can avoid surprises, choose better coverage, and ensure you are properly protected in case of an accident.

Frequently Asked Questions

What is the most important part of a car insurance policy?

The declarations page, because it summarizes your coverage, limits, and deductibles.

Why are insurance policies so hard to read?

They are legal documents written to be precise and avoid ambiguity.

What should I check first in my policy?

Start with coverage limits, deductibles, and exclusions.

Can I change my insurance policy after signing it?

Yes, most policies can be adjusted or updated at any time.