Types of Car Insurance Coverage Explained (Liability vs Full Coverage)

Car insurance in the United States is built around different types of coverage, each designed to protect drivers from specific financial risks. However, many people misunderstand what these coverages actually include, especially the difference between liability insurance and full coverage.

Choosing the wrong type of coverage can lead to paying too much for insurance or, worse, being underinsured in case of an accident. This guide breaks down the main types of car insurance coverage in simple terms and explains exactly how they work in real situations.

Understanding the structure of car insurance coverage

Car insurance is not a single product but a combination of different coverage types that can be added or removed depending on your needs.

Most policies are built around a base requirement (liability insurance) and then expanded with optional protections such as collision or comprehensive coverage.

The two most important concepts to understand are:

- Liability insurance (minimum legal requirement in most states)

- Full coverage insurance (a combination of multiple protections)

These are not official technical categories, but rather practical terms used by insurers and drivers.

What is liability insurance?

Liability insurance is the most basic form of car insurance and is required by law in almost every U.S. state.

Its purpose is simple: it covers damages and injuries you cause to other people if you are responsible for an accident.

Liability insurance is divided into two main parts:

Bodily injury liability

This covers medical expenses, rehabilitation costs, and sometimes legal fees if you injure another person in an accident.

Property damage liability

This covers the cost of repairing or replacing another person’s vehicle or property that you damage in an accident.

However, liability insurance does NOT cover:

- Your own vehicle repairs

- Your medical expenses

- Theft or vandalism of your car

This means that while liability insurance keeps you legally compliant, it does not protect your own financial loss in many situations.

What is full coverage car insurance?

Full coverage is not a single type of insurance, but rather a combination of several coverages that protect both you and others.

Typically, full coverage includes:

- Liability insurance

- Collision coverage

- Comprehensive coverage

Because of this combination, full coverage provides significantly broader protection compared to liability-only insurance.

Collision coverage explained

Collision coverage pays for damage to your own vehicle after an accident, regardless of who is at fault.

This includes situations such as:

- Colliding with another vehicle

- Hitting a stationary object like a pole or guardrail

- Single-car accidents (for example, losing control of the vehicle)

Collision coverage is especially important for newer or more expensive vehicles, where repair costs can be significant.

However, it usually comes with a deductible, which is the amount you must pay before the insurance covers the rest.

Comprehensive coverage explained

Comprehensive coverage protects your vehicle from non-collision-related damage. This type of coverage applies to situations that are often unpredictable or outside your control.

Common examples include:

- Theft of your vehicle

- Vandalism or intentional damage

- Fire damage

- Weather-related events such as hailstorms or floods

- Animal collisions (such as hitting a deer)

Comprehensive insurance is particularly valuable in areas with high theft rates or extreme weather conditions.

Liability vs full coverage: key differences

The main difference between liability insurance and full coverage comes down to what is protected.

Liability insurance only covers damage you cause to others. It does not protect your own vehicle.

Full coverage, on the other hand, includes protection for both your own car and others involved in an accident.

In practical terms:

- Liability insurance = minimum legal protection

- Full coverage = financial protection for your own vehicle as well

Another major difference is cost. Liability insurance is significantly cheaper, while full coverage can be several times more expensive depending on the vehicle and driver profile.

When liability insurance is enough

Liability insurance may be sufficient in certain situations.

It is commonly used when:

- The vehicle is old or has low market value

- The cost of full coverage exceeds the value of the car

- The driver wants to minimize monthly expenses

In these cases, paying for full coverage may not be financially efficient, since repair costs could exceed the car’s value.

When full coverage is recommended

Full coverage is generally recommended when the vehicle has significant value or replacement costs would be high.

It is especially useful for:

- New cars

- Financed or leased vehicles (often required by lenders)

- High-value or luxury cars

- Drivers who want maximum financial protection

In these cases, full coverage helps avoid large out-of-pocket expenses after an accident or unexpected event.

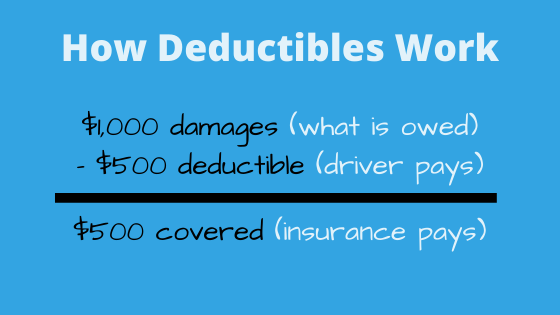

The role of deductibles in full coverage

Both collision and comprehensive coverage usually include a deductible.

This is the amount the policyholder must pay before the insurance company contributes to the claim.

For example:

- Damage cost: $2,000

- Deductible: $500

- Insurance pays: $1,500

Choosing a higher deductible typically lowers the monthly premium, while a lower deductible increases the cost of insurance.

Why full coverage is more expensive

Full coverage costs more because it protects against a wider range of risks.

Insurance companies calculate premiums based on potential payouts. Since full coverage includes damage to your own vehicle, the insurer takes on more financial risk.

Factors that increase the cost of full coverage include:

- Vehicle value and repair costs

- Driver age and experience

- Location and accident rates

- Driving history

Common misconception about “full coverage”

One of the most common misunderstandings is that “full coverage” means everything is covered in every situation.

In reality, full coverage is still subject to:

- Policy limits

- Deductibles

- Exclusions in the contract

For example, full coverage does not automatically include rental car reimbursement, roadside assistance, or gap insurance unless explicitly added.

Do you really need full coverage?

The decision depends on balancing risk and cost.

A useful rule of thumb is:

- If your car is new or expensive → full coverage is usually worth it

- If your car is older and low value → liability may be enough

However, personal financial situation also matters. Some drivers prefer full coverage for peace of mind, even if their car is not new.

Final thoughts

Understanding the difference between liability and full coverage is essential for making informed decisions about car insurance in the United States.

Liability insurance keeps you legally protected but offers limited financial protection for your own vehicle. Full coverage, while more expensive, provides a much higher level of security against accidents, theft, and unexpected damage.

Choosing the right option depends on your vehicle’s value, your budget, and your tolerance for financial risk.

Frequently Asked Questions

Is full coverage car insurance required in the USA?

No, but lenders often require it if the car is financed or leased.

What does liability insurance not cover?

It does not cover your own vehicle, your injuries, or non-liability damage.

Is full coverage worth it for older cars?

Often not, if the car’s value is low compared to the insurance cost.

Can I switch from full coverage to liability?

Yes, but only if you fully own the vehicle and it is not financed.