What Happens After a Car Accident? (Step-by-Step Insurance Claim Process 2026)

A car accident is a stressful and often confusing experience, especially when it comes to dealing with insurance companies afterward. Many drivers are unsure about what steps to take, how claims work, and what their insurance actually covers in real situations.

Understanding the post-accident process is essential because it directly affects how quickly your vehicle gets repaired, whether your medical expenses are covered, and how much you may need to pay out of pocket.

This guide explains step by step what happens after a car accident in the United States, how the insurance claim process works, and what you should do at each stage to protect yourself financially and legally.

Step 1: Ensure safety and check for injuries

Immediately after an accident, the first priority is safety. Before thinking about insurance or responsibility, it is essential to check if anyone is injured.

If possible:

- Move vehicles out of traffic if it is safe to do so

- Turn on hazard lights

- Check yourself and passengers for injuries

- Call emergency services if needed

Even in minor accidents, it is important to take the situation seriously, as some injuries may not be immediately visible.

Step 2: Contact the police

In many states, it is required or strongly recommended to contact the police after an accident, especially if there are injuries or significant damage.

A police officer will:

- Document the scene

- Collect statements from both drivers

- Create an official accident report

This report is extremely important for your insurance claim, as it provides an official record of what happened and may help determine fault.

Step 3: Exchange information with the other driver

After ensuring safety and contacting authorities, drivers must exchange essential information.

This includes:

- Full name and contact details

- Insurance company and policy number

- Driver’s license number

- Vehicle information (make, model, license plate)

It is also recommended to take photos of:

- Vehicle damage

- The accident scene

- Road conditions and traffic signs

This evidence can be very useful during the claims process.

Step 4: Notify your insurance company

You should report the accident to your insurance company as soon as possible. Most insurers allow you to file a claim through:

- Mobile app

- Website

- Phone call

When reporting the accident, you will need to provide:

- Date, time, and location

- Description of what happened

- Information about other parties involved

- Photos and police report (if available)

Prompt reporting helps speed up the claims process and prevents delays.

Step 5: Claim investigation begins

Once the claim is filed, the insurance company begins its investigation. This is one of the most important stages of the process.

During this phase, the insurer will:

- Review all submitted information

- Analyze police reports

- Contact witnesses if necessary

- Assess vehicle damage

The goal is to determine:

- Who was at fault

- What coverage applies

- How much compensation is needed

Step 6: Assignment of an insurance adjuster

In more complex cases, the insurance company assigns an insurance adjuster.

The adjuster is responsible for:

- Inspecting the damaged vehicle

- Estimating repair costs

- Evaluating claim validity

- Determining settlement amounts

In some cases, the adjuster may meet you in person or request that the vehicle be taken to an approved repair shop for inspection.

Step 7: Fault determination

One of the most critical parts of the claims process is determining fault.

Fault can be:

- Clear (one driver is fully responsible)

- Shared (both drivers share responsibility)

- Disputed (requires further investigation)

Fault determination affects:

- Whose insurance pays

- Whether your deductible applies

- How your insurance rates may change

In disputed cases, the process may take longer and involve additional evidence review.

Step 8: Repair estimate and approval

Once damage is assessed, the insurance company provides a repair estimate.

This estimate includes:

- Cost of parts

- Labor costs

- Repair time

After review, the insurer either:

- Approves repairs at an authorized shop

- Issues a payment for repairs

- Declares the vehicle a total loss if repair costs are too high

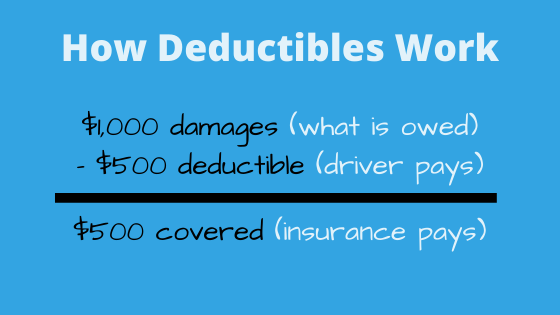

Step 9: Deductible payment

If your policy includes a deductible (collision or comprehensive coverage), you will need to pay this amount before the insurance covers the remaining cost.

For example:

- Total repair cost: $3,000

- Deductible: $500

- Insurance pays: $2,500

The deductible is typically paid directly to the repair shop or deducted from the final payout.

Step 10: Vehicle repair or settlement

Once everything is approved, the final stage begins.

There are two possible outcomes:

Vehicle repair

Your car is repaired at an approved body shop. The insurance company pays the repair costs directly or reimburses you depending on the arrangement.

Total loss settlement

If repair costs exceed the vehicle’s value, the insurance company declares it a total loss and pays you the actual cash value of the car, minus any deductible.

Step 11: Claim closure

After repairs or payment are completed, the insurance company closes the claim.

At this point:

- All payments are finalized

- Documentation is stored in your insurance record

- The claim is considered resolved

However, the claim may still affect your future insurance rates depending on fault and severity.

How long does the claims process take?

The duration of a car insurance claim can vary depending on complexity.

- Simple claims: a few days to one week

- Moderate claims: 1–3 weeks

- Complex or disputed claims: several weeks or longer

Factors affecting timing include:

- Severity of damage

- Availability of police reports

- Cooperation between drivers

- Insurance company processing speed

How claims affect your insurance rate

Filing a claim, especially if you are at fault, can lead to an increase in your insurance premium.

However, not all claims affect rates equally:

- At-fault accidents → likely increase

- No-fault accidents → may not affect rates (depends on state)

- Comprehensive claims → often minimal impact

Insurance companies evaluate risk based on your driving history over time.

Common mistakes after a car accident

Many drivers make mistakes that negatively affect their claim:

- Not taking photos of the accident scene

- Admitting fault too early

- Delaying the insurance report

- Not collecting full information from the other driver

- Accepting verbal agreements without documentation

Avoiding these mistakes can significantly improve your claim outcome.

Final thoughts

The process that follows a car accident in the United States can seem complicated, but it follows a clear and structured system designed to evaluate damage, assign responsibility, and provide financial compensation.

Understanding each step of the insurance claim process helps drivers act correctly in stressful situations, avoid delays, and ensure they receive fair compensation.

From the moment an accident happens to the final claim settlement, every step plays a role in determining how quickly and effectively your insurance support is delivered.

Being prepared and informed is one of the best ways to protect yourself financially on the road.

Frequently Asked Questions

What should I do immediately after a car accident?

Check for injuries, ensure safety, and contact emergency services if needed.

Do I need to call the police after an accident?

In most cases, yes, especially if there are injuries or significant damage.

How long does an insurance claim take?

It can range from a few days to several weeks depending on complexity.

Will my insurance go up after an accident?

It depends on fault, claim type, and your insurance history.