Why Your Car Insurance Rates Went Up (and How to Fix It)

Seeing your car insurance premium increase can be frustrating, especially if you have not made any changes to your policy or driving habits. However, insurance rate increases are very common in the United States, and they are usually the result of multiple factors rather than a single cause.

Insurance companies regularly adjust pricing based on risk data, claims trends, inflation, and personal driving history. This means your premium can go up even if you personally have not had an accident.

Understanding why your car insurance rates increased is the first step to controlling them and potentially lowering your costs again.

1. You were involved in an accident

One of the most common reasons for an increase in insurance rates is being involved in an accident, especially if you were at fault.

When you file a claim, insurance companies consider you a higher risk driver. This is because statistical data shows that drivers who have been in accidents are more likely to be involved in future incidents.

Even a single at-fault accident can cause:

- Higher monthly premiums

- Loss of safe driver discounts

- Reclassification into a higher risk category

The impact usually lasts for several years, depending on the insurance company and state regulations.

2. Traffic violations or tickets

Speeding tickets, reckless driving charges, or other traffic violations can significantly increase your insurance costs.

Insurance companies use your driving record to assess risk. Violations suggest a higher probability of future claims, which leads to higher premiums.

Common violations that increase rates include:

- Speeding tickets

- Running red lights

- Distracted driving (e.g., phone use)

- DUI or DWI offenses

Even minor violations can affect your insurance for multiple years.

3. Increased claims in your area

Sometimes your insurance rates increase even if your personal record is clean.

This happens because insurance companies adjust pricing based on regional risk. If your area experiences more accidents, thefts, or severe weather events, insurers may raise premiums for all drivers in that region.

Factors that influence regional increases include:

- Higher accident frequency

- Increased vehicle theft rates

- Severe weather damage (hail, floods, storms)

- Rising repair costs in your area

This means your ZIP code can directly affect your insurance price.

4. Inflation and rising repair costs

Modern vehicles are more expensive to repair than ever before due to advanced technology such as sensors, cameras, and electronic systems.

When repair costs increase, insurance companies adjust premiums to maintain profitability.

Key factors include:

- Higher cost of auto parts

- Labor shortages in repair shops

- Increased medical costs after accidents

- Supply chain disruptions

Even if your driving record remains unchanged, rising industry costs can still increase your premium.

5. Changes in your credit score

In many U.S. states, insurance companies use credit-based insurance scores to help calculate premiums.

If your credit score drops, your insurance rate may increase because insurers associate lower credit scores with higher risk profiles.

Factors that can affect your credit score include:

- Late payments

- Increased debt usage

- Missed financial obligations

Improving your credit score can help reverse insurance increases over time.

6. Changes in your policy or coverage

Sometimes insurance rates go up simply because your policy has changed.

This may include:

- Increased coverage limits

- Lower deductible selection

- Added optional coverages (rental car, roadside assistance, etc.)

Even small adjustments can increase your monthly premium significantly.

It is important to review your policy carefully when it renews to understand what has changed.

7. Loss of discounts

Many insurance discounts are temporary or conditional. If you no longer qualify, your rate may increase automatically.

Common reasons include:

- No longer qualifying for a safe driver discount

- Graduation (loss of student discount)

- Changes in household or marital status

- Removing bundled policies

Losing discounts can have a major impact on your final premium.

8. Adding a new driver or vehicle

If you add a new driver to your policy, especially a young or inexperienced driver, your insurance rate will likely increase.

Similarly, adding a new vehicle can change your risk profile depending on:

- Vehicle type

- Value

- Repair costs

- Safety rating

Teen drivers and high-performance vehicles usually cause the biggest premium increases.

9. Insurance company pricing adjustments

Insurance companies periodically adjust their pricing models based on overall market performance.

Even if your personal risk has not changed, your insurer may increase rates due to:

- Higher claim payouts across the company

- Changes in underwriting strategy

- Regulatory changes in your state

- Market competition shifts

This is one of the least controllable reasons for rate increases.

10. You moved to a new location

Relocating can significantly impact your insurance premium.

Insurance companies calculate risk based on ZIP code, and moving to a new area can change your rate due to:

- Traffic density

- Accident statistics

- Crime rates

- Weather conditions

Even moving a few miles can result in noticeable differences in price.

How to reduce your car insurance after a rate increase

Even if your insurance has gone up, there are several strategies to reduce it again.

Compare insurance providers

Different companies calculate risk differently, so switching providers can lead to immediate savings.

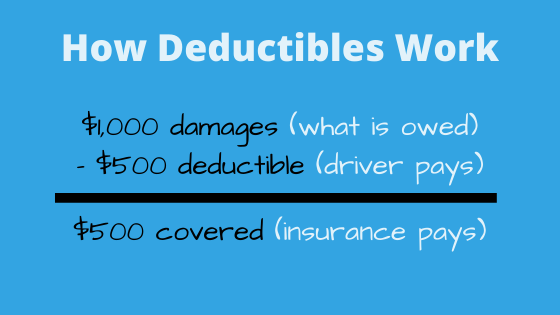

Increase your deductible

A higher deductible reduces monthly premiums, but increases out-of-pocket costs after a claim.

Review your coverage

Remove unnecessary add-ons that do not provide value for your situation.

Ask for discounts

Many drivers miss out on available discounts simply because they do not ask.

Improve your driving record

Over time, maintaining a clean record can help lower your rates again.

Can you avoid insurance rate increases?

Not all increases can be avoided, but many can be minimized by:

- Driving safely and avoiding violations

- Maintaining a good credit score

- Reviewing your policy annually

- Comparing quotes regularly

- Choosing vehicles wisely

Insurance pricing is dynamic, but proactive management can help keep costs under control.

Final thoughts

Car insurance rate increases are common in the United States and are usually caused by a combination of personal, regional, and economic factors.

While some increases are unavoidable, many can be reduced or reversed by understanding how insurance companies calculate risk and adjusting your policy accordingly.

Being proactive, comparing options, and maintaining good driving and financial habits are the most effective ways to keep your insurance costs stable over time.

Frequently Asked Questions

Why did my car insurance go up for no reason?

Often due to regional risk changes, inflation, or company-wide pricing adjustments.

How long does an accident affect insurance rates?

Usually between 3 to 5 years, depending on the insurer.

Can I negotiate my car insurance rate?

Not directly, but you can reduce it by adjusting coverage or switching providers.

Does credit score really affect insurance rates?

Yes, in most U.S. states it is a key pricing factor.